Fintech

One of the biggest challenges for fintech companies is navigating the complex regulatory environment, says Altron FinTech.

Fintech

Perfect payment experience: Why offering multiple options is key to business success

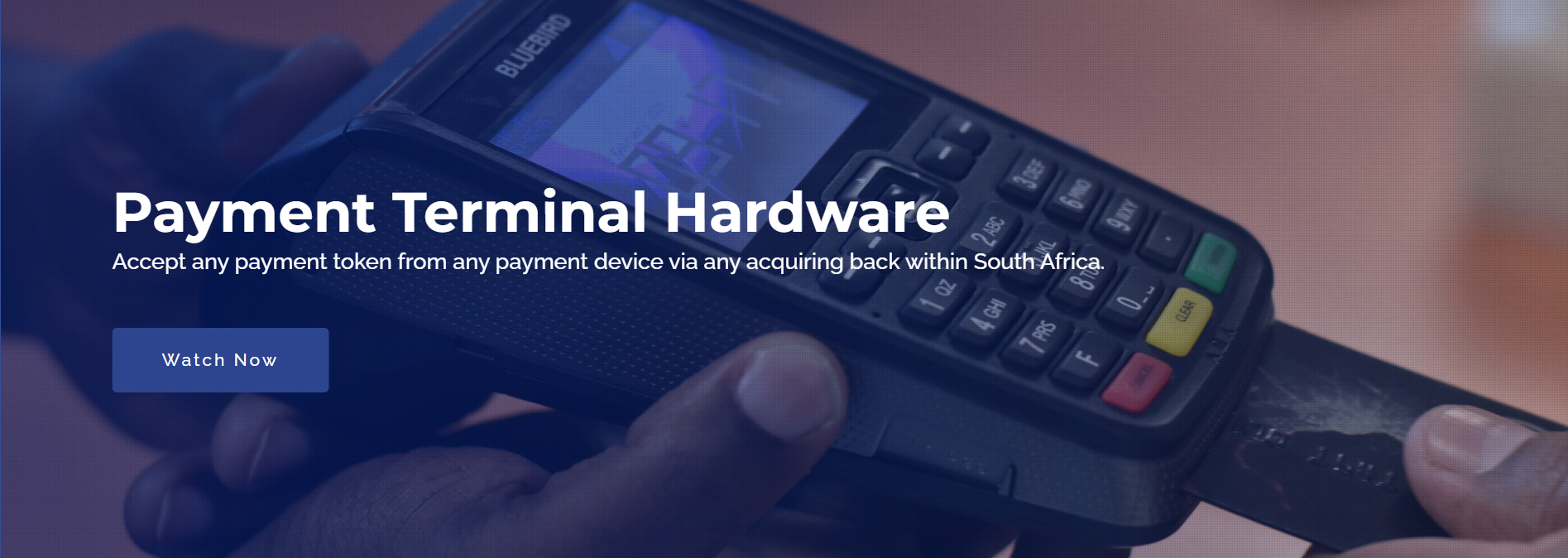

Merchants must accept any payment token their customers prefer, says Altron FinTech.

Fintech

Securing digital transactions with Altron FinTech ACS

Tokenisation using a token service provider is a process in which sensitive data, such as credit card numbers, is replaced with a unique identifier or token.

Financials

Altron FinTech Household Resilience Index confirms negative impact of high interest rates on household debt costs

Arguably the most worrying trend in the latest AFHRI is the year-on-year decline of 8.7% in the ratio of household income to debt costs.