BlackBerry may be up for sale: CEO Thorsten Heins has hinted the company could be open to offers.

Nothing much has changed at BlackBerry HQ since the last time we wrote about the Canadian company's difficulties - it's still in decent financial shape and has new products to try to win back some credibility, if not actual glory - but relentless pressure from the market may be encouraging the board to consider exit strategies while there is still good value in the firm.

If BlackBerry does go up for sale, the eventual buyer will cause ripples throughout the industry.

A new owner will raise questions of the future path for enterprise services, at a time when IT departments are wrestling with mobile security, device management and BYOD.

The slow (re)start

In January, the BlackBerry 10 operating system debuted, along with the first smartphone in the revamped BlackBerry stable - the touch-screen Z10. That was rapidly followed by the Q10, sporting the traditional BlackBerry keyboard layout, and more recently the lower-spec Q5 has arrived, aiming at the cost-conscious segment in which BlackBerry is still strong, particularly in emerging markets like SA.

We've also had the comprehensive overhaul of BlackBerry Enterprise Server, the messaging platform for corporate environments.

But in the half-year since the arrival of BB10, BlackBerry has struggled for traction. The new phone models are selling, but competitors are selling more. A lot more.

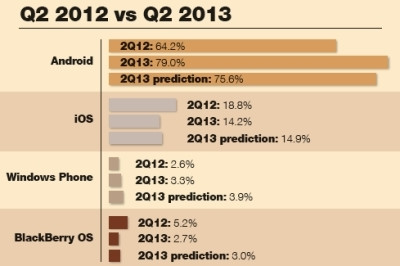

Gartner's forward projection for smartphone market share showed Android growing, iOS slowing, Microsoft nibbling out a niche, and BlackBerry shrinking. The confirmed Q2 numbers show that the trends were correct, but underestimated:

Android has grown faster than expected, iOS slowed more sharply, Microsoft grew a little slower than expected, and BlackBerry shrunk beyond expectations. BlackBerry's share has dropped nearly 50% since Q2 last year, from 5.2% to 2.7%. Heins hoped to hit the ground running, but it looks like the company may have slipped coming out of the blocks. Lay-offs in the R&D department, following a separate big redundancy last year, haven't helped reassure the market of the company's prospects either.

Although the company is selling plenty of phones, the tiny market share makes it a tough sell to app developers, and in the smartphone world, if you haven't got the apps, you haven't got a future.

What's for sale

BlackBerry as a company has much more in its portfolio than just the phones. The intellectual property, comprising 5 000 active patents and almost as many applications, primarily in the mobile space, is a valuable commodity, for a start. Many acquisitions are driven heavily by IP, like Google's purchase of Motorola for $13 billion. Nortel's patents were sold for $4.5 billion, when the former telecoms giant went to the wall, to a consortium including Apple, Microsoft... and BlackBerry.

The enterprise messaging platform still has traction, and the mobile device management space is becoming very focused on security, where BlackBerry still enjoys a strong reputation. The global network behind BlackBerry services also has great potential in the right hands. And the firm has about $3 billion in cash, which raises its value.

Altogether, analysts peg the selling price of the company at about $10 billion. That's really not a lot, in context - plenty of possible suitors could put that sort of money on the table, in cash or shares. But that assumes the company would be sold intact. A very real possibility is that it could be broken up, like Nortel, and sold off in pieces. That could fetch a higher aggregate price, which might appease shareholders.

Given the spread of assets and options, potential buyers are a mixed group of large firms with broad interests, focused players who would want specific parts. There are a lot of possibilities - we'll just look at some of the key players and most likely candidates.

Who's buying?

Several device manufacturers would be contenders. Samsung and Apple continue to dominate the handset market, and it is entirely possible that a smaller rival might look to use BlackBerry to boost its share. That is a risky strategy, especially when the incoming technology is on the way down, but BlackBerry has enough key technologies, like its security framework and messaging platform, for a buyer to see value in the deal.

Lenovo, for example, has already suggested it would be willing to put an offer on the table. Lenovo wants to improve its position in the mobile space and has failed to achieve much traction against the Apple/Samsung juggernaut. ZTE is also a possibility - another manufacturer struggling to establish its products outside its home territory, though the strategic fit is questionable.

But Lenovo and ZTE share a common problem: they are Chinese. The online animosity between Western powers and China are reaching Cold War levels, and the acquisition of a key telecoms player - one with an incumbent presence in government departments and corporate boardrooms, access to messaging data and e-mail flowing over its servers, and security technology - by a Chinese entity is almost unthinkable. If the Canadian government didn't move to quash that possibility, the US government would apply every possible ounce of pressure on its northern neighbour to ensure no deal progressed beyond speculation.

Blocking the Chinese

The roll-call of possible suitors is long, but few are real candidates

BlackBerry itself (going private): definitely a possibility, and would buy the company breathing space to develop its strategy away from the quarterly scrutiny of shareholders and analysts.

Private equity (split it up and sell the parts): probably unlikely unless the company hits serious financial difficulty, but definitely an option in that instance. That'd be the end of BlackBerry as we know it.

Amazon: No. Terrible strategic fit, unless Bezos has some breathtaking strategic surprise in mind.

Dell: Unlikely - none of BlackBerry's core assets align to Dell strategy.

Facebook: Surprisingly strong outsider, with much to gain even though it would be a big risk given the size of the deal.

Google: Might bid just to stir up trouble, but probably not interested in acquisition.

HP: Hopefully not. Palm, webOS, and now BlackBerry? It would end badly.

HTC: An outlier - not a great strategic fit and the size of the deal would be tough for HTC to digest.

Huawei: No. Great strategic fit, but Chinese with close links to government, so absolutely no chance of regulatory go-ahead.

Lenovo: No. Already expressed interest, but being Chinese is unlikely to see regulatory approval.

LG: Unlikely. Needs a mobile boost, but one failing mobile brand buying another is not a winning combination.

Microsoft: Not impossible, just unlikely. Redmond would like the MDM and messaging tech, and the patents.

Nokia: No chance. Too closely tied to Microsoft to move out of Redmond's shadow.

Samsung: Strong contender. Needs the patents, the messaging and the security.

ZTE: No. Relatively poor strategic fit, and Chinese to boot, so no chance of a green light.

Yahoo: Possible, but unlikely to be a happy marriage.

Acquisitions of US firms are subject to approval by the Committee on Foreign Investment in the US (CFIUS), a regulatory body that has repeatedly nixed high-tech deals, particularly those with security implications. And not just the Chinese: Israeli security firm Check Point tried to buy SourceFire (an intrusion detection company) in 2005 - no dice. Huawei has seen several US deals blocked, and its board has openly stated that the company has effectively given up on trying to acquire US firms. BlackBerry, being Canadian, is not subject to CFIUS, but the Canadian government has similar oversight, and pays close attention to the demands of the US.

Which also means, of course, that Huawei is not an option for BlackBerry either and that is a deal with great strategic possibilities. Huawei not only manufactures devices (and would like to fare better against Samsung on the world stage), but telecoms transmission equipment too.

BlackBerry Services, fully integrated into the Huawei telecoms kit, have great potential - Huawei has telecoms customers all around the world, especially in emerging markets where BlackBerry still enjoys robust market share. There are excellent prospects for a Huawei/BlackBerry tie-up, but there is absolutely no chance such a deal would meet with regulatory approval.

Huawei has even been accused of providing the Chinese government with access to telecoms data. It denies those claims, but of all the impossible Chinese suitors for BlackBerry, Huawei is the least likely of them all.

HTC might be able to get away with it, being Taiwanese. Like HTC, it would stand to gain from BlackBerry's reputation, technology and market presence. HTC manufactures high-quality products but has struggled to achieve results against Samsung's saturation marketing. $10 billion would be a big bite for HTC, though, and it is questionable whether it could turn the fading fortunes of a Canadian manufacturer into strategic value.

Korean muscle

While Chinese firms face stiff opposition to any acquisition, Koreans are on far more amicable terms - the nation is an ally of the West, and any regulatory concern would be more likely to centre on market dominance than political differences.

Two obvious contenders present themselves: LG and Samsung. LG is as bad a strategic fit as HTC - the company needs a boost in mobile, but buying a dying brand is not the way to achieve it.

Samsung clearly needs no help in the smartphone market. The company is streets ahead of its rivals, with 31.7% share of Q2 sales. The nearest rival, Apple, managed only 14.2%, and third place was LG, with 5.1%. In fact, Samsung outsells the rest of the top five combined, so BlackBerry's addition to the pie would barely register. But it's not all roses for Samsung - it wants to break into the messaging space to strengthen ties with network operators, but its own platform, ChatOn, has not yet delivered the numbers despite being pre-installed on all Samsung devices.

Fold ChatOn into BBM and suddenly the Korean giant would have a messaging footprint comparable to its handset dominance. And the biggest gap in Samsung's portfolio is device management and security. The firm is building out its products - SAFE and KNOX - to shore up its security offering, but BlackBerry's existing, and well-established, security portfolio would fit in very nicely, strengthening Samsung's enterprise position against Microsoft. The addition of BlackBerry's patent portfolio would also be hugely welcome - Samsung and Apple are engaged in a bitter patent feud, with the Koreans on the back foot. A Samsung acquisition would be hitching the BlackBerry wagon to a dragster.

Other manufacturers have strategic problems

Of the other manufacturers, Nokia is another option, but that's not really an option at all. Nokia has problems of its own - its dramatic fall from grace has mirrored BlackBerry's - but it's tied itself to Microsoft's coat-tails and there's no chance of that changing, not with ex-Microsoft exec Stephen Elop heading the Finnish manufacturer. Anyway, Nokia is taking tentative steps back to viability - Windows Phone is slowly carving out a niche and Nokia is dominating it. Adding BlackBerry to its baggage would only weigh Nokia down.

Ironically, while Nokia is too tied to Microsoft to consider an acquisition, Microsoft itself could be interested. Microsoft has a strong existing interest in enterprise messaging, and adding BlackBerry's suite to the mix would make it even more powerful, at a time when the enterprise server market is increasingly more important to the firm's income as the PC market declines.

On the hardware side of things, Dell is an unlikely candidate. Although mobile is an important part of the firm's strategy, it's far more focused on management, not handsets, with emphasis on the data centre. Laptops and tablets have not been the core of Dell's strategy for years: phones would be entirely off book.

HP is more likely, but the company burned its fingers with Palm, then did it all over again with webOS. It would take an astounding degree of chutzpah to convince the shareholders to bet $10 billion on yet another failing mobile OS. If it does happen, it's unlikely to end well.

Online and out of the box

All these candidates are existing players, but there's a market segment with plenty of cash and a propensity for surprise acquisitions: the Web giants. If any of the traditional manufacturers were to buy BlackBerry, the results would probably be a predictable merging of device lines, rebranding of services and possibly some patent litigation, but probably no curve-balls. But what if a nouveau-riche Web darling were to make an offer?

Jeff Bezos, after all, just stumped up a quarter of a billion for a newspaper. Is it possible that Amazon might eye BlackBerry? The company is, after all, in the mobile device market now with the Kindle range. Actually, no, it's not likely at all. Amazon might have a hugely diversified market presence but its product strategy is laser-focused, and BlackBerry wouldn't fit in.

Google is more likely, for all the wrong reasons. If Microsoft expresses interest, Google probably will too. Not that Larry Page actually wants BlackBerry - the search giant is still digesting its $12 billion 2012 acquisition of Motorola, and doesn't really need any part of BlackBerry - it is enjoying near-saturation in mobile, both through the growing dominance of Android and the pervasive reach of its search, video and mapping apps. Page would probably bid just to get the price up, though, just as he did to annoy the telecoms incumbents when US spectrum went to the auction block in 2008.

Yahoo is more likely: Marissa Miller knows she needs to take dramatic steps to restore the company to the lustre of its early Internet days. The company has a messaging presence, and plenty of business content, so it's not inconceivable. But there is much discontent among Yahoo staff, with reports of infighting and projects left to languish - it is hard to see BlackBerry thriving in such an atmosphere.

Our last candidate is the surprise package, a firm with plenty of cash, a willingness to make big acquisitions, a strategic focus on at least part of BlackBerry's core business, and the drive to win. We're talking about Facebook.

Facebook has finance aplenty after its IPO raised $16 billion and gained it a market cap of (at the time of writing) just a hair under $94 billion (and on its way back up after the rocky post-IPO period). The company dropped a cool billion dollars for Instagram despite the photo service being worth not a fraction of that price (hint: the value's in the long-term strategy and the value of dominating photo-sharing social networking).

The company is also desperate to dominate mobile - it knows that users are increasingly mobile but its ad revenue is not, and it's on a campaign to address that (with signs of success, too). But its efforts to promote "Facebook Home", a launcher that basically replaces a smartphone's interface with a Facebook skin, met poor reception and was widely panned, but the company has not given up. Buying BlackBerry would give it a complete environment under its control - there's probably nothing Zuckerberg wants more.

At the same time, it would give the company a big boost in enterprise credibility and a strong messaging platform to strengthen its position against rivals, notably Google. Chances are the portfolio would remain largely unchanged for the foreseeable future - no sense scaring off the few enterprise users who remain - but BlackBerry OS 11 might look very different. For consumers, who love messaging and social media and can't really be bothered about the enterprise features, that could be an attractive proposition. For enterprise users, it could be less convincing, but the possibility of a Facebook tie-up is still intriguing.

Other options

BlackBerry could go private, similar to the process currently under way at Dell. Taking the company private would mean it can draw a discreet veil over its performance indicators, focusing instead on articulating, and delivering, a long-term strategy. From a corporate perspective, that makes sense. Whether it could reverse the downward momentum of the actual product line is questionable.

Or the company could be taken apart. Private equity could step in, buy up the firm and then break it up for parts, selling the components for a combined profit.

That would be the end of BlackBerry as we know it, but it might be the best financial result for shareholders.

This is all speculation, but for BlackBerry's enterprise users, the company going up for sale could have deep implications. Any acquirer will hasten to reassure customers that existing products will continue to be supported, of course, but some will be nervous regardless. Some, conversely, may be excited about the prospects of the one-time smartphone leader's future, under the umbrella of Samsung, HTC or, yes, even Facebook.

Share