Although traditional banks have retained their advantage of established trust relationships with customers, advancing digital disruption will erode profitability unless they can respond.

Gary Stocks, an executive at BSG responsible for research and insights, advises that global revenue from digital banking products and services is estimated to grow to almost half of banks' revenue over the next five years. "Fintechs and challenger banks often have an IT cost per user that is 10% that of traditional banks1."

In South Africa, despite banks having invested heavily in IT, the expected efficiency and scale benefits have not been realised, with the cost-to-income ratios of the major banks stubbornly sitting at around 55% between 2013 to 20152. "There are many causes of this such as the cost to hire and retain scarce skills, slowing revenue growth, increasing spend on compliance and the cost to maintain expensive legacy technology platforms. But the underlying problem is a failure to respond to changing consumer behaviour," comments Stocks.

He believes what is important is understanding what needs to be done to address the interplay between digital and physical in the emerging digitised business and consumer world:

1. Accept the digital transformation.

2. Change the architecture perspective to one of an ecosystem, with customers at the centre and customer experience the starting point.

3. Move from a project to a product mind-set.

Accept the digital transformation

Stocks says there has been no lack of investment in digital capabilities among the large banks in South Africa, for example:

* The four largest banking groups all have mobile apps, with FNB Mobile on 1.5 million devices as at September 2015.

* Standard Bank has acquired SnapScan, one of a number of innovative payment solutions developed by start-ups.

* Merchants in the business banking sector can use mobile point-of-sale acquiring devices, such as ABSA's Payment Pebble.

* Nedbank has released a merchant dashboard to provide insight to a small business' typical cash flow management challenge.

* FNB, ABSA and Standard Bank have all released contactless card payment instruments, one step closer to mobile card-based payment solutions.

The imperative, according to Stocks, is to impact profitability by moving from building tools to enterprise transformation. "This is similar to the lesson from Capitec's customer-focused strategy, which resulted in product simplification, a stark contrast to the increasing product complexity displayed by the larger banks," he says.

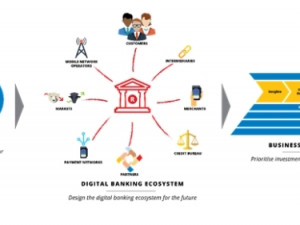

The approach represented in the model below starts with behavioural-based customer research, to identify more personalised strategies, to inform the design of the ecosystem and the enabling business capabilities. In Africa, mobile is key, given the growth in mobile penetration to over 80% and global growth of 25% in mobile broadband3.

Banks becoming ecosystems

Banks have traditionally built their business capabilities themselves, suggests Stocks. "The future for banks in a resource-limited environment such as Africa, is to identify which parts of the ecosystem they want to build and own, and which parts they want to rent. A good example of this exists in the micro-insurance sector with MTN Ghana, Hollard Insurance, MicroEnsure and MFS Africa collaborating on 'mi-Life', launched in Ghana in 2011."

From an IT perspective, this means building operating platforms and digital capabilities at the business-customer interface to support this ecosystem. It means moving from distinct applications to building open platforms that integrate internally and externally, with management of business processes separated from application logic, and integrated data management and analytics capabilities.

Delivering business capabilities and not discrete projects

Traditionally, change is delivered through discrete projects, which need to compete for funding each year. This approach offers limited incentives to build digital products and services that deliver sustained benefits. Benefits are not usually measured because the project team has disbanded by the time these are realised. There is no time to optimise the architecture of the digital capabilities and the organisation becomes burdened with technical debt, accrued through the cost of support and maintenance teams.

Stocks believes leaders of change must apply the concept of a product lifecycle to digital products and services, providing multi-year funding; to enable teams to increase their productivity as they understand the domain and work together to deliver benefits and not simply digital capabilities.

"Start by focusing on the team and not individual skills. This means moving away from managing pools of people such as business analysts and software developers and moving towards building multi-functional teams, where individual success is tied to team success and team success is tied to benefits realisation, rather than simply meeting artificial time and cost deadlines."

References

1. 2016 CIO Agenda: A Financial Services Perspective, 19 February 2016, David Furlonger, Gartner

2. Resilient through changing times: Major banks analysis - South Africa, 15 September 2015, PwC

3. Ericsson Mobility Report, February 2016, MWC Edition

About the author

An executive responsible for research and insights, Gary Stocks is passionate about unlocking potential and accelerating performance at BSG's clients and people. His focus is on creating value in an increasingly digital world through customer-centric thinking and data-driven insights.

Share

BSG

BSG is an African consulting and technology company with 20 years' experience across the banking, specialised financial services, insurance, telecommunications and oil and gas sectors. Bridging the gap between business and IT, BSG gets it done with its clients by enabling business and IT leaders to work together to solve important business problems. By unlocking potential, BSG can accelerate performance for clients, while growing the client's people. Journeying with clients from needs to results, BSG utilises fact-based decision-making to design practical solutions to deliver business benefits quickly. Visit it at www.bsg.co.za.

Editorial contacts