Share

About IHS Towers

IHS Towers is one of the largest independent owners, operators and developers of shared communications infrastructure in the world by tower count and is a leading independent multinational telecommunications infrastructure provider of scale to solely focus on global emerging markets. The Company has nearly 39,000 towers pro forma across its 11 markets: Brazil, Cameroon, Colombia, Côte d’Ivoire, Egypt, Kuwait, Nigeria, Peru, Rwanda, South Africa and Zambia. For more information, please email: communications@ihstowers.com or visit: www.ihstowers.com

Cautionary statement regarding forward-looking Information

This press release contains forward-looking statements. We intend such forward-looking statements to be covered by relevant safe harbor provisions for forward-looking statements (or their equivalent) of any applicable jurisdiction, including those contained in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical facts contained in this press release may be forward-looking statements. In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “targets,” “projects,” “contemplates," “believes,” “estimates,” “forecast,” “predicts,” “potential” or “continue” or the negative of these terms or other similar expressions. Forward-looking statements contained in this press release include, but are not limited to statements regarding our future results of operations and financial position, including our anticipated results for the fiscal year 2022, industry and business trends, business strategy, plans, market growth and our objectives for future operations.

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. Forward-looking statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements, including, but not limited to:

- non-performance under or termination, non-renewal or material modification of our customer agreements;

- volatility in terms of timing for settlement of invoices or our inability to collect amounts due under invoices;

- a reduction in the creditworthiness and financial strength of our customers;

- the business, legal and political risks in the countries in which we operate;

- general macroeconomic conditions in the countries in which we operate;

- changes to existing or new tax laws, rates or fees;

- foreign exchange risks and/or ability to access U.S. Dollars in our markets;

- regional or global health pandemics, including COVID 19, and geopolitical conflicts and wars, including the current situation between Russia and Ukraine;

- our inability to successfully execute our business strategy and operating plans, including our ability to increase the number of Colocations and Lease Amendments on our Towers and construct New Sites or develop business related to adjacent telecommunications verticals (including, for example, relating to our anticipated fiber businesses in Latin America and elsewhere) or deliver on our sustainability or environmental, social and governance (ESG) strategy and initiatives including plans to reduce diesel consumption;

- reliance on third-party contractors or suppliers, including failure or underperformance or inability to provide products or services to us (in a timely manner or at all) due to sanctions regulations, due to supply chain issues or other reasons;

- increases in operating expenses, including increased costs for diesel;

- failure to renew or extend our ground leases, or protect our rights to access and operate our Towers or other telecommunications infrastructure assets;

- loss of customers;

- changes to the network deployment plans of mobile operators in the countries in which we operate;

- a reduction in demand for our services;

- the introduction of new technology reducing the need for tower infrastructure and/or adjacent telecommunication verticals;

- an increase in competition in the telecommunications tower infrastructure industry and/or adjacent telecommunication verticals;

- our failure to integrate recent or future acquisitions;

- reliance on our senior management team and/or key employees;

- failure to obtain required approvals and licenses for some of our sites or businesses or comply with applicable regulations;

- environmental liability;

- inadequate insurance coverage, property loss and unforeseen business interruption;

- compliance with or violations (or alleged violations) of laws, regulations and sanctions, including but not limited to those relating to telecommunications regulatory systems, tax, labor, employment (including new minimum wage regulations), unions, health and safety, antitrust and competition, environmental protection, consumer protection, data privacy and protection, import/export, foreign exchange or currency, and of anti-bribery, anti-corruption and/or money laundering laws, sanctions and regulations;

- fluctuations in global prices for diesel or other materials;

- disruptions in our supply of diesel or other materials;

- legal and arbitration proceedings;

- reliance on shareholder support (including to invest in growth opportunities) and related party transaction risks;

- risks related to the markets in which we operate;

- injury, illness or death of employees, contractors or third parties arising from health and safety incidents;

- loss or damage of assets due to security issues or civil commotion;

- loss or damage resulting from attacks on any information technology system or software;

- loss or damage of assets due to extreme weather events whether or not due to climate change;

- failure to meet the requirements of accurate and timely financial reporting and/or meet the standards of internal control over financial reporting that support a clean certification under the Sarbanes Oxley Act;

- risks related to our status as a foreign private issuer; and

- the important factors discussed in the section titled “Risk Factors” in our Annual Report on Form 20-F for the fiscal year ended December 31, 2021.

The forward-looking statements in this press release are based upon information available to us as of the date of this press release, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements. You should read this press release and the documents that we reference in this press release with the understanding that our actual future results, performance and achievements may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements. These forward-looking statements speak only as of the date of this press release. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained in this press release, whether as a result of any new information, future events or otherwise.

Use of Non-IFRS financial measures

Certain parts of this press release contain non-IFRS financial measures, including Adjusted EBITDA, Adjusted EBITDA Margin, Recurring Levered Free Cash Flow (“RLFCF”) and Consolidated RLFCF. The non-IFRS financial information is presented for supplemental informational purposes only and should not be considered a substitute for financial information presented in accordance with IFRS, and may be different from similarly titled non-IFRS measures used by other companies.

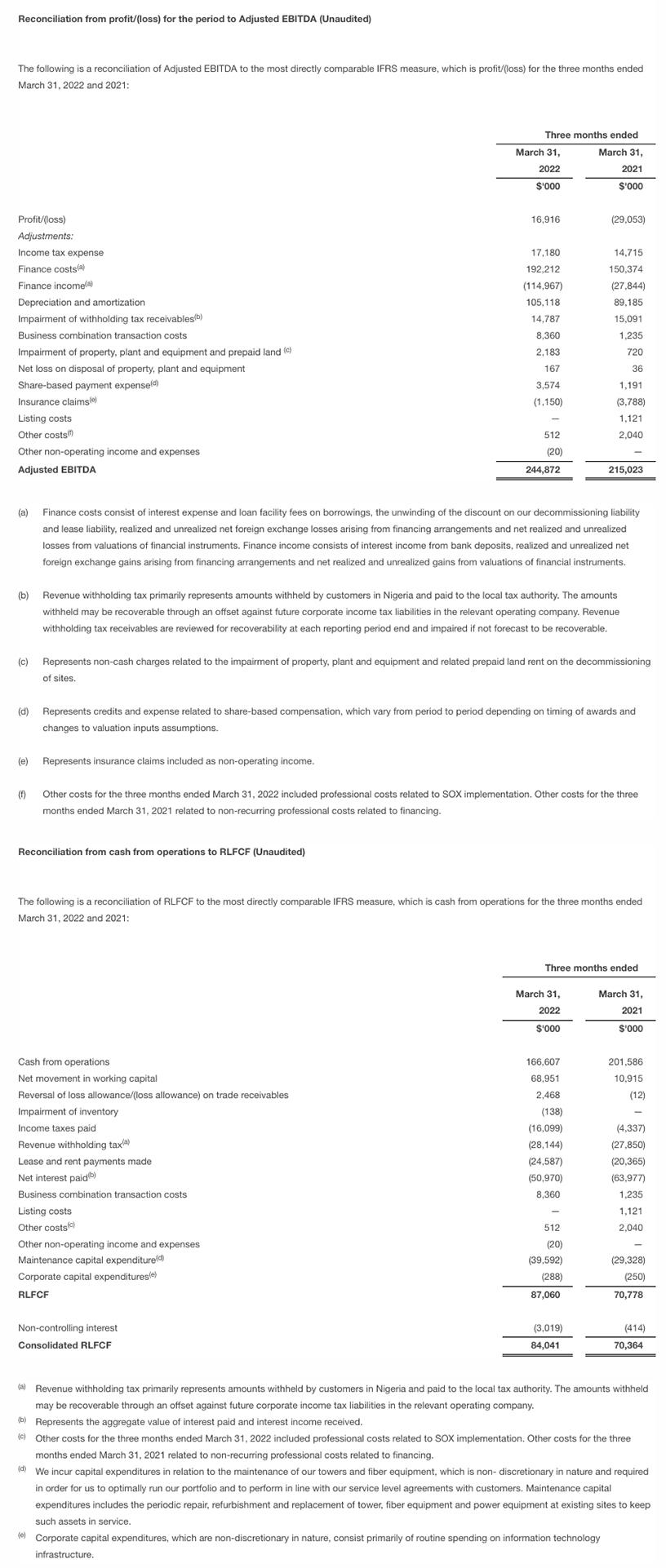

We define Adjusted EBITDA as profit/(loss) for the period, before income tax expense/(benefit), finance costs and income, depreciation and amortization, impairment of withholding tax receivables, business combination transaction costs, impairment of property, plant and equipment and related prepaid land rent on the decommissioning of sites, net (profit)/loss on sale of assets, share-based payment (credit)/expense, insurance claims, listing costs and certain other items that management believes are not indicative of the core performance of our business. The most directly comparable IFRS measure to Adjusted EBITDA is our profit/(loss) for the period.

Segment Adjusted EBITDA (defined as profit/(loss) for the period, before income tax expense/(benefit), finance costs and income, depreciation and amortization, impairment of withholding tax receivables, business combination transaction costs, impairment of property, plant and equipment and related prepaid land rent on the decommissioning of sites, net (profit)/loss on sale of assets, share based payment (credit)/expense, insurance claims, costs relating to this offering and certain other items that management believes are not indicative of the core performance of its business)) to assess the performance of the business.

We define Adjusted EBITDA Margin as Adjusted EBITDA divided by revenue for the applicable period, expressed as a percentage.

We believe that Adjusted EBITDA is an indicator of the operating performance of our core business. We believe Adjusted EBITDA and Adjusted EBITDA Margin, as defined above, are useful to investors and are used by our management for measuring profitability and allocating resources, because they exclude the impact of certain items which have less bearing on our core operating performance. We believe that utilizing Adjusted EBITDA and Adjusted EBITDA Margin allows for a more meaningful comparison of operating fundamentals between companies within our industry by eliminating the impact of capital structure and taxation differences between the companies.

Adjusted EBITDA measures are frequently used by securities analysts, investors and other interested parties in their evaluation of companies comparable to us, many of which present an Adjusted EBITDA-related performance measure when reporting their results.

Adjusted EBITDA and Adjusted EBITDA Margin are used by different companies for differing purposes and are often calculated in ways that reflect the circumstances of those companies. You should exercise caution in comparing Adjusted EBITDA and Adjusted EBITDA Margin as reported by us to Adjusted EBITDA and Adjusted EBITDA Margin as reported by other companies. Adjusted EBITDA and Adjusted EBITDA Margin are unaudited and have not been prepared in accordance with IFRS.

Adjusted EBITDA and Adjusted EBITDA Margin are not measures of performance under IFRS and you should not consider Adjusted EBITDA or Adjusted EBITDA Margin as an alternative to profit/(loss) for the period or other financial measures determined in accordance with IFRS.

Adjusted EBITDA and Adjusted EBITDA Margin have limitations as analytical tools, and you should not consider them in isolation. Some of these limitations are:

- they do not reflect interest expense, or the cash requirements necessary to service interest or principal payments, on our indebtedness;

- although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often need to be replaced in the future and Adjusted EBITDA and Adjusted EBITDA Margin do not reflect any cash requirements that would be required for such replacements;

- some of the items we eliminate in calculating Adjusted EBITDA and Adjusted EBITDA Margin reflect cash payments that have less bearing on our core operating performance, but that impact our operating results for the applicable period; and

- the fact that other companies in our industry may calculate Adjusted EBITDA and Adjusted EBITDA Margin differently than we do, which limits their usefulness as comparative measures.

Accordingly, prospective investors should not place undue reliance on Adjusted EBITDA or Adjusted EBITDA Margin.

We believe that it is important to measure the free cash flows we have generated from operations, after accounting for the cash cost of funding and recurring capital expenditure required to generate those cash flows. In this respect, we monitor RLFCF which we define as cash from operations, before certain items of income or expenditure that management believes are not indicative of the core performance of our business (to the extent that these items of income and expenditure are included within cash flow from operating activities), and after taking into account loss allowances on trade receivables, impairment of inventory, net working capital movements, net interest paid or received, revenue withholding tax, income taxes paid, lease payments made, maintenance capital expenditures, and routine corporate capital expenditures.

We believe RLFCF are useful to investors because they are also used by our management for measuring our operating performance, profitability and allocating resources. While Adjusted EBITDA provides management with a basis for assessing its current operating performance, in order to assess the long-term, sustainable operating performance of our business through an understanding of the funds generated from operations, we also take into account our capital structure and the taxation environment (including withholding tax implications), as well as the impact of non- discretionary maintenance capital expenditures and routine corporate capital expenditures, to derive RLFCF. RLFCF provides management with a metric through which to measure how the underlying cash generation of the business by further adjusting for expenditures that are non-discretionary in nature (such as interest paid and income taxes paid), as well as certain non-cash items that impact profit/(loss) in any particular period.

RLFCF measures are frequently used by securities analysts, investors and other interested parties in their evaluation of companies comparable to us, many of which present an RLFCF-related performance measure when reporting their results. Such measures are used in the telecommunications infrastructure sector as they are seen to be important in assessing the long-term, sustainable operating performance of a business. We present RLFCF to provide investors with a meaningful measure for comparing our cash generation performance to those of other companies, particularly those in our industry.

RLFCF, however, are used by different companies for differing purposes and are often calculated in ways that reflect the circumstances of those companies. You should exercise caution in comparing RLFCF as reported by us to RLFCF or similar measures as reported by other companies. RLFCF are unaudited and have not been prepared in accordance with IFRS.

RLFCF are not intended to replace profit/(loss) for the period or any other measures of performance under IFRS, and you should not consider RLFCF as an alternative to cash from operations for the period or other financial measures as determined in accordance with IFRS. RLFCF have limitations as analytical tools, and you should not consider these in isolation. Some of these limitations are:

- not all cash changes are reflected, for example, changes in working capital are not included and discretionary capital expenditures are not included;

- some of the items that we eliminate in calculating RLFCF reflect cash payments that have less bearing on our core operating performance, but that impact our operating results for the applicable period;

- the fact that certain cash charges, such as lease payments made, can include payments for multiple future years that are not reflective of operating results for the applicable period, which may result in lower lease payments for subsequent periods;

- the fact that other companies in our industry may have different capital structures and applicable tax regimes, which limits its usefulness as a comparative measure; and

- the fact that other companies in our industry may calculate RLFCF differently than we do, which limits their usefulness as comparative measures.

Accordingly, you should not place undue reliance on RLFCF.

View source version on businesswire.com: https://www.businesswire.com/news/home/20220517005332/en/

Contacts

Media:

Sard Verbinnen & Co

Email: IHS-SVC@sardverb.com

Investor Relations:

InvestorRelations@ihstowers.com