Mobile subscriber growth in Sub-Saharan Africa has slowed in recent years as the industry confronts the challenges of affordability and a youthful population.

This is according to a recent GSM Association (GSMA) report, The Mobile Economy Sub-Saharan Africa 2018, which suggests future growth opportunities will increasingly be concentrated in rural and low-ARPU (average revenue per user) markets, as well as younger demographic groups.

World Bank data indicates around 40% of the population in Sub-Saharan Africa is under the age of 16, a demographic segment that has significantly lower levels of mobile ownership compared to the population as a whole.

"The industry is also facing challenges in terms of affordability as it attempts to connect incremental subscribers, with economic volatility and political instability in a number of countries potentially exacerbating challenges around purchasing power and low disposable incomes," the report reads.

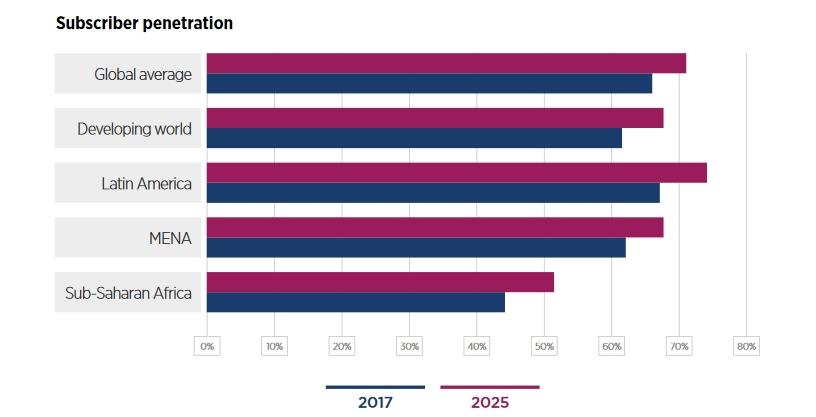

Network economics can also prove challenging for mobile operators looking to connect populations in rural and remote regions. As a result of these issues, GSMA predicts Sub-Saharan Africa will remain the least penetrated region to 2025, with the gap compared to global average figures reducing only modestly over the forecast period.

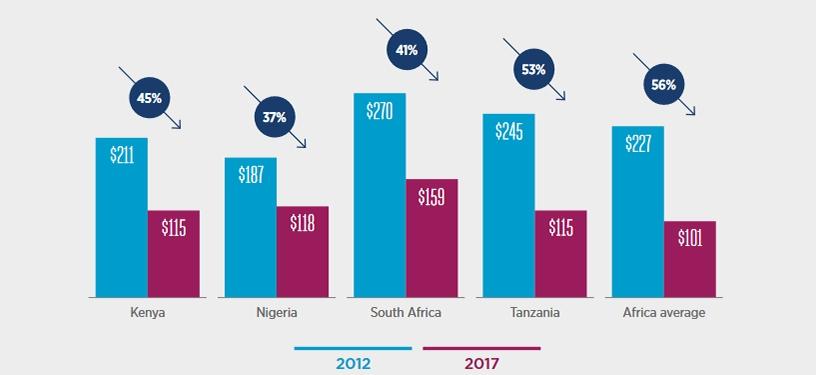

Affordability represents a significant barrier to the uptake of mobile services in the region, with the total cost of mobile ownership (TCMO) determined by the cost of service usage (voice, data, SMS), activation and mobile handset. GSMA says countries in Sub-Saharan Africa have among the highest level of TCMO as a proportion of income worldwide; this is particularly pronounced for those at the bottom of the income pyramid.

For the 27 countries in the region where data is available, the TCMO for purchasing a handset and 500MB of data per month represents on average 10% of monthly income, well above the 5% threshold recommended by the UN Broadband Commission.

In many markets across the region, handset cost and sector-specific taxes, such as SIM taxes imposed on consumers and mobile operators, also affect the affordability of devices and services.

Meanwhile, the declining cost of smartphones is allowing more people to access high-speed mobile Internet services. The average selling price of smartphones has fallen below $120 (R1 738) in most markets, with sub-$100 smartphones, mostly from Asian manufacturers such as Gionee and Tecno, now widely available across the region.

Penetration rates

The report found that although subscriber growth in the region has slowed in recent years, Sub-Saharan Africa's rates still remain well ahead of global averages.

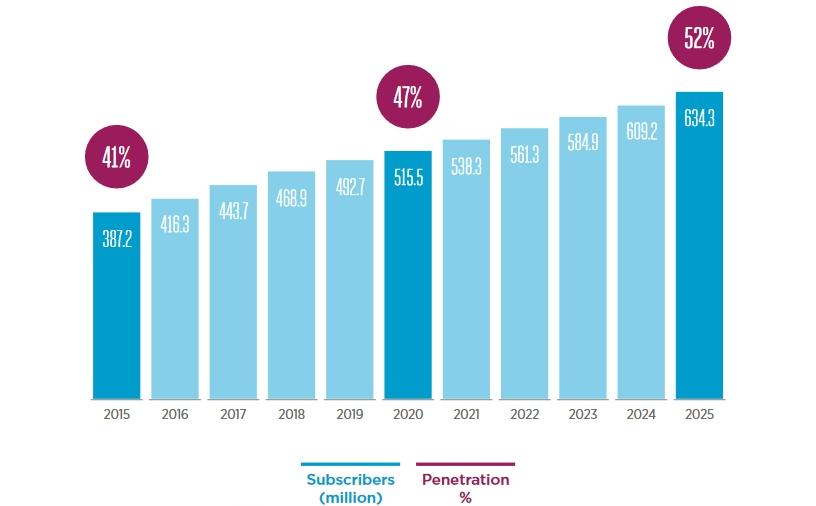

The regional subscriber base will grow at a compound annual growth rate (CAGR) of 4.8% for the period 2017-2022, more than double the global growth rate over the same period. However, growth rates in Sub-Saharan Africa have fallen well below the double-digit annual growth rates seen in the first half of the decade, and the CAGR for the next five years is roughly half the level recorded over the preceding five years.

As a result, GSMA predicts penetration rates will see only modest increases from current levels. The penetration rate is forecast to reach 50% by the end of 2023, and 52% by 2025.

"The issue of slowing subscriber growth at a time when less than half the population have a mobile subscription highlights both the opportunity and the challenge that the mobile industry faces in the region in terms of connecting new subscribers," the report says.

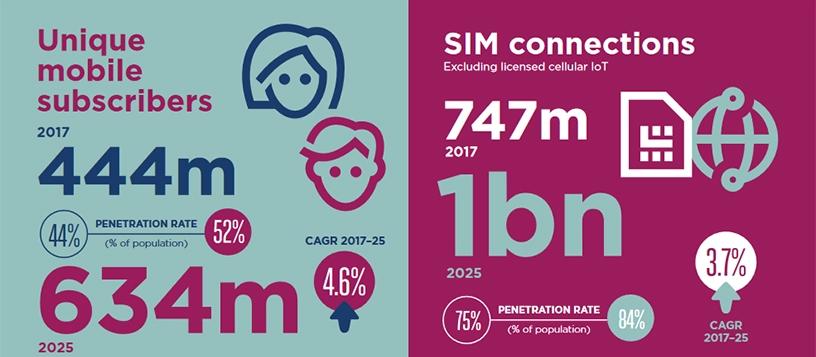

Unique mobile subscriber penetration in Sub-Saharan Africa stood at 44% at the end of 2017, well below the global average of 66%. The subscriber base in the region totalled 444 million, equivalent to around 9% of total global subscribers.

There were around 747 million SIM connections in the region at the end of 2017 (excluding licensed cellular IOT, which represented a further 16 million). This figure will increase to just over one billion by 2025, according to GSMA, taking connections penetration in the region from 75% to 84% by 2025.

The report found that levels of multi-SIM ownership have declined in recent years and will continue to fall modestly. This reflects a range of factors, including more stringent regulations on SIM registration, improving network quality and reduced opportunities for price arbitrage.

Smartphone progress

GSMA says smartphone adoption continues to see rapid growth in the region, albeit from a relatively low base and despite affordability challenges. The total number of smartphone connections stood at 250 million at the end of 2017, equivalent to around a third of the total connections base.

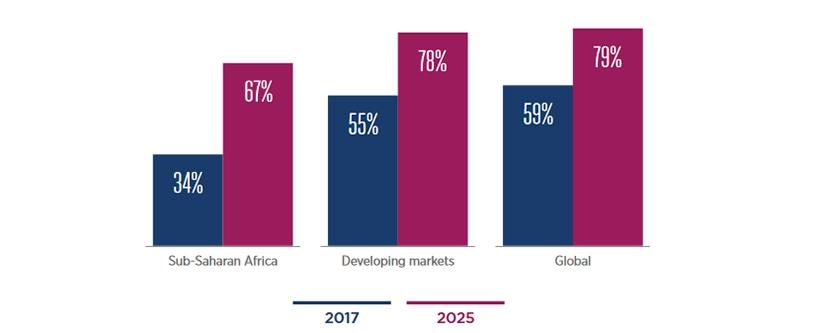

The adoption rate will double by 2025 to reach two-thirds of total connections, equivalent to an installed base of around 690 million. Rapid growth in the number of smartphones in the region means the adoption gap compared to the developing market average will close materially over the forecast period.

Smartphone adoption is helping to drive strong growth in data traffic across the region, although mobile operators will face challenges in monetising the ongoing data traffic growth amid regulatory moves to reduce out-of-bundle charges and ongoing competitive pressures.

A key driver of smartphone adoption is the growth of entry-level devices at affordable prices, often from more price-focused brands, including the likes of China's Shenzhen Transsion Holdings. The company sells phone in the region under the Tecno and other brands, with its sales accounting for close to a third of the region's total market.

GSMA says Chinese players have traditionally dominated the feature phone market in Africa but are now increasingly active in the smartphone market, though Samsung remains a leading player in this market segment.

Share