5G rollouts continue to challenge fibre for new customers in the South African market.

This is according to local market analyst firm BMIT’s latest SA Broadband Report, which highlights the escalating tussle for customers between fibre and 5G fixed wireless access providers, as key players in both technologies invest in coverage expansion.

Chris Geerdts, MD of BMIT, says there has been unprecedented investment in residential fibre in recent years, although a few large players did take a breather in 2023.

Meanwhile, 5G rollouts continue to challenge fibre for new customers, after investment was partially diverted into mitigating the severe impacts of load-shedding, battery theft and vandalism.

He notes mobile operators are also adding coverage and capacity to their LTE networks, with fixed-LTE still by far the leading broadband medium in South Africa – by coverage and subscriber numbers.

Telkom has periodically alternated between prioritising fibre and mobile network investments, but is now investing in both, and tailoring its 5G/LTE/fibre mix to the data needs of each suburb. It is selling its tower assets to fund the updated strategy, says the market analyst firm.

It notes that customers are the ultimate beneficiaries of these investments, with the combined growth in active broadband connections projected by BMIT to grow at a CAGR of 9.1% between 2022 and 2027.

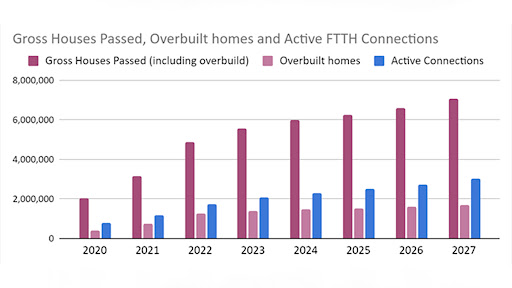

A good portion of those connections will come from fibre, as shown below in BMIT’s baseline forecast scenario, which projects active connections reaching just under three million by 2027.

As the chart shows, BMIT says houses passed in that timeframe will reach seven million, in the context of an ongoing fibre “land grab”, which has extended for more than a decade, and has now expanded to several fronts.

It explains that the competitive intensity in the most lucrative suburbs has resulted in overbuild – where operators deploy fibre in streets which another operator has already passed. As the above chart shows, it adds, an estimated 25% of homes are already overbuilt.

However, the most significant growth in the last few years has been in the next tier of metro suburbs and secondary cities and many towns, although last year saw a slow down by a few key players, albeit temporarily, the firm says.

BMIT forecasts ongoing deployment of access fibre in both the residential and business market, saying it will now be far more focused in the lower average revenue per user market cohorts.

“This will require investors to show confidence in the emerging new business models tailored for the ‘township economy’, incorporating innovative go-to-market models along with lower-cost network deployment techniques,” BMIT states.

“These are either prepaid or pay-as-you-go services, with price points as low as R5 per day or R100 per month.”

It points out that examples are prepaid models from new entrants, such as Fibertime in Stellenbosch, Zing Fibre in Umlazi and Ilitha in Mdantsane, along with challenges from mainstream fibre operators, such as Vuma with its ‘Key’ offering, Frogfoot with Rise and Openserve with Prepaid Connect.

“The projects are currently characterised as ‘pilot projects’, although Fibertime has already commenced with expansion to other areas in Cape Town, stating that its proof-of-concept project in Kayamandi, Stellenbosch, has been successful and the business case is now proven.”

Geerdts notes 5G rollouts are continuing to challenge fibre for new customers, particularly in areas where fibre has yet to be deployed.

“The pace of rollout has been negatively impacted by load-shedding, as mobile operators were forced to divert funds to boost battery capacity at sites, as well as to protect these sites from battery theft and vandalism, but operators are now once again focusing on accelerating 5G expansion,” he says.

“Overall 5G population coverage passed 30% in South Africa last year, with the main focus being to provide fixed-wireless services in urban areas. Rain still has the highest coverage and is expanding as funds allow.”

Maximising LTE

Meanwhile, the report states mobile operators are adding coverage and capacity to their LTE networks, with fixed-LTE still by far the leading broadband medium in South Africa – both in terms of network coverage and actual subscriber numbers.

The LTE market is mature and operators are still in the process of maximising their deployment of the spectrum they acquired in 2022. They are also paving the way for the ‘sunsetting’ of their 2G and 3G networks, although BMIT anticipates 2G services will remain available in some form for years to come.

Low earth orbit satellite services are in focus now and regarded as potentially disruptive to the market, says BMIT.

It notes that OneWeb services are available in SA via BCX and QKon, but priced for the business market.

Starlink has around 2.3 million subscribers globally, but is not yet licensed to operate in SA. BMIT’s view is that the equipment and services are currently too expensive to suggest there will be mass uptake in the near future.

It believes that fixed-4G/5G adoption will likely be sustained by aggressively-priced uncapped and quasi-uncapped offerings, supported by the ever-reducing cost of 5G devices.

Share