South Africa’s wholesale telecoms market is expected to see phenomenal growth, spurred by the fibre industry.

This is one of the biggest takeaways from local market analyst firm BMIT’s latest SA Wholesale Telecoms Report. It projects healthy growth in SA’s fibre industry over the next five years.

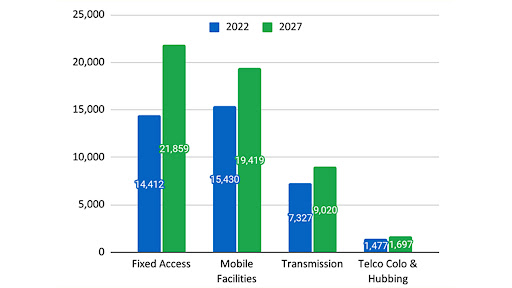

The company expects the combined wholesale telecoms market to deliver a compound annual growth rate (CAGR) of 6.1% to reach R52 billion in 2027.

BMIT anticipates the wholesale fixed access market will reach a 9.1% CAGR by 2027, and will soon overtake mobile facilities in revenue.

It says this wholesale fixed access revenue derives mainly from the fibre network operators (FNOs) that have transformed the urban broadband access market in 10 years.

Chris Geerdts, MD of BMIT, says this growth is a tribute to South African entrepreneurship in the face of substantial headwinds.

He says the industry was also wise to adopt an open access model, which has proven itself in so many other countries across the world. “This model allows the FNOs to focus on rolling out infrastructure, while the internet service providers focus on sales and customer support services.”

While fibre deployment has been nothing short of a “land grab” since 2014, BMIT says it has noted accelerated growth in the past two years, driven by renewed investment in the rollout of access fibre in the residential segment (FTTH), including rapid deployment in second-tier cohorts and selected middle- to lower-income, high-density urban areas.

Geerdts says much of the next wave of FTTH coverage growth is expected to come from rollout projects in third-tier cohorts by new and existing players.

He notes these projects are largely still in pilot mode, in which new, innovative, business models are being tested.

According to BMIT, the projected growth, therefore, depends on how feasible these projects prove to be, as that impacts investor confidence.

“Obviously operators connecting lower-income areas need to connect higher numbers of houses to maintain their revenue growth,” Geerdts says.

The market analyst firm says mobile wholesale is still SA’s largest wholesale telecoms market, worth R15.4 billion per annum.

While the fibre market was open access from the start, it notes, the mobile market is opening slowly.

The firm explains that much of the revenue in this market is derived from active network sharing between operators, as Vodacom and MTN could not get access to LTE spectrum for over 10 years and so entered into wholesale agreements with smaller mobile operators to supplement network capacity.

Following the 2022 spectrum auction, these large operators are investing in their own networks.

“Therefore, growth in the active network sharing market will come more from the capacity that smaller operators lease from MTN and Vodacom. 5G may also catalyse new sharing agreements in time.”

It points out that mobile operators around the world are selling off their mobile tower assets to mobile tower companies for various reasons, including unlocking cash to invest in network expansion and reducing costs.

“Mobile tower companies generally operate on an open access basis, which results in better utilisation of their sites, as they seek to attract multiple customers to share each tower.

“An added requirement in SA is that mobile towers need to provide extended power backup due to load-shedding, while vandalism and battery theft at sites continue to plague the industry, and investors are showing greater interest in sustainable energy sources,” the firm says.

It notes Telkom was the first operator to separate its tower assets and is actively seeking investment into that entity.

Last year, the passive infrastructure market was dominated by MTN’s tower carve-out with IHS (completed in June 2022) which includes provision for IHS providing power-as-a-service to MTN, it states.

Meanwhile, it adds, Vodacom has formed a subsidiary tower, to own and operate its towers, as the largest tower company within the country.

“As operators increase their LTE capacity and rollout 5G, the demand for mast space and for new sites continues to increase, while the orderly shutdown of legacy (2G and 3G) services will allow the removal of older, less efficient equipment. Each site requires backhaul transmission, which is ideally provided by fibre, where feasible, to support the gigabit data speeds needed for LTE and 5G sites.”

According to BMIT, recent government focus on legislation and regulation has been on opening the mobile market to greater competition, particularly at the wholesale level.

The draft Electronic Communications Amendment Bill has been published for public response and includes a range of proposed updates, including the introduction of a licence category for providing facilities services.

There are also specific measures to promote the mobile virtual network operator (MVNO) industry, says the firm.

“This MVNO industry represents a smaller component of mobile wholesale overall, but BMIT sees significant potential for growth. While new entrants, such as Melon Mobile, aim to offer innovative new services, most of the large retailers (such as Shoprite) and the banks (including FNB, Standard Bank and Capitec) see the potential to offer convergent (mobile and financial) services.”

Cable considerations

BMIT believes the recent landing of three high-capacity cables in South Africa (Equiano, 2Africa and PEACE) will bring substantial capacity to SA, while offering choice to the local market and improving resilience through route diversity.

“In some cases, better latency can be expected. The national routes between cities are now all served by multiple operators with dark fibre, leading to a robust wholesale market, with greatly increased capacity and reduced pricing, while the push by FNOs to smaller towns has extended demand beyond the cities,” Geerdts says.

BMIT expects this market to grow to just over R9 billion by 2027.

Telco colocation and hubbing

Teraco pioneered the carrier-neutral model in data centres in 2008, and soon became the dominant player in the wholesale market, further assuring its popularity in 2012, by providing free peering between customers, says BMIT.

It comments that this entrenched Teraco’s market position and became a catalyst for new service development, because businesses can create secure, fast and reliable connections to customers, service providers and partners via peering, at relatively low cost.

ZA-INX continues to grow as a multi-site, neutral peering alternative, it says.

The firm notes new players in the past 24 months include Vantage Data Centres – with Oracle also expanding capacity.

“WIOCC’s business, Open Access Data Centres is focusing on providing edge data centre facilities interconnected with larger centres. NTT and Liquid are also making significant plays in SA and across Africa.

BMIT sees this market reaching a 2.8% CAGR by 2027.

“Overall, FTTH has been, and will continue to be the key contributor to SA’s wholesale telecoms market. This market has been open access from the start, while Teraco introduced the carrier-neutral model as the catalyst for growth in the data centre market.

“The mobile facilities market is gradually opening to new players and greater competition, with government seeking to open this market further,” it concludes.

Share