Constant bouts of load-shedding and the rise in over-the-top (OTT) services are accelerating the decline in traditional voice calls in South Africa.

This is according to market analyst firm BMIT’s SA Voice Services and UC&C Report, which projects a continuing, steep decline in call volumes and revenue across the fixed and mobile voice services markets, while anticipating exceptional growth in emerging unified communications and collaboration (UC&C) services.

It reveals the telecoms voice services sector experienced a steep decline in 2022, with a particularly harsh impact from load-shedding.

Over the years, South Africa has suffered severe power cuts as embattled power utility Eskom struggles to keep the lights on.

Telco operators have been lamenting the adverse effects of the rolling blackouts, which they say impact network quality. The telcos have been spending billions of rands to mitigate the chaos caused by load-shedding.

The power outages have also resulted in vandals and thieves increasingly targeting telco base stations while using the cover of darkness.

According to a recent report by US-based broadband testing diagnostics firm Ookla, load-shedding is having a massive impact on SA’s mobile performance.

Embracing the new

Chris Geerdts, BMIT managing director, says UC&C services are disrupting traditional telephony just as Uber disrupted the metered taxi industry.

“Customers want the benefits of high-definition calls, conferencing, video and multimedia, as well as the ability to send and receive messages and posts when it suits them,” he says.

“Customers hardly think twice nowadays when using OTT apps such as WhatsApp and Telegram, to communicate individually or with a range of personal, family and business groups. Similarly, platforms such as Microsoft Teams and Slack have become indispensable daily tools at work.”

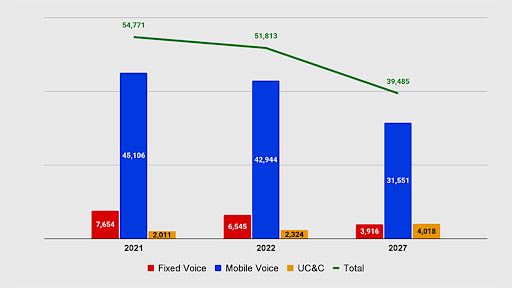

However, from an industry standpoint, the revenue from UC&C is still well below that of voice, as seen in BMIT’s market summary chart for the past two years (shown below), along with a forecast for 2027, highlighting the uneven growth per sector.

BMIT explains that as the chart shows, the telephony industry has been hard hit in the past year, with mobile cell sites experiencing significantly higher levels of down-time due to power outages and battery theft, which had the effect of blocking fixed and mobile calling to mobile phones.

However, it notes, even if load-shedding was to end, or at least the impact was mitigated by operators beefing up the power resilience in their networks, the disruptive long-term trend of ongoing substitution of traditional voice calling by alternative communication styles would still remain intact.

“With fixed voice, the legacy PSTN [public switched telephony network] market has been in decline for over 20 years in South Africa, initially impacted by a shift from fixed to mobile usage,” says BMIT.

“Next-generation voice-over-IP (VOIP) services have also been eroding the PSTN market, and these services are slightly more resilient to the longer-term rate of decline. The fixed voice category on the chart shows their combined revenue.”

The firm adds that much of the UC&C revenue is attributed to cloud-hosted PBX and collaboration platforms, such as Microsoft Teams.

The category has seen a healthy increase of 21% in CAGR over the past three years, but this growth only offsets the rate of decline of the total by 0.7% in each year, due to its much lower weighting in the overall services “basket”.

BMIT’s forecast for UC&C is 11.6% CAGR through 2027, reaching R4 billion.

The market analyst firm points out that the longer-term disruptive trend of a decline of origination voice traffic in South Africa mirrors the global trend.

The UK, for example, already experienced a 14% decline in fixed-line and 2% decline in mobile traffic in 2021, as reported by the UK communications regulator, Ofcom.

The sub-trends include ongoing fixed-mobile substitution, and recently also a decline in mobile calling, both of which have been amplified by the acceleration in OTT voice/multimedia usage during the COVID-19 pandemic, it explains.

“While OTT voice and multimedia usage are general trends impacting traditional voice calling, especially in the B2C segment, UC&C is having an equally significant impact on the B2B market.”

No going back

BMIT believes cloud-hosted communication platforms have reshaped the tariffed voice routing landscape globally, and are making a similar impact in South Africa.

It notes these range from basic cloud-hosted exchanges (PBXs) to systems with a rich UC&C feature-set and, in some cases, integration with other productivity and enterprise resource planning or customer relationship management platforms (through APIs).

“Microsoft Teams, generally procured through Microsoft 365 licences, made a massive impact during the COVID-19 pandemic, stimulated initially by Microsoft offering free Teams usage,” says the firm.

It observes that many companies are strongly invested in the Microsoft ecosystem and will have top-of-the range corporate Microsoft 365 licences that include components that enable breakout directly from Teams to fixed and mobile networks.

“The largest growth opportunity in cloud communication platforms, as seen by local players, lies in cloud-hosted PBXs, this being the largest market in revenue terms currently, and one which is still growing at 20% per annum in respect of cumulative active user licences.

“All leading voice players have this type of product offering, the growth of which mitigates, somewhat, the general maturation in their tariffed voice services revenues. However, even for most VOIP-focused players, tariffed voice is still a significantly larger revenue component than their UC&C revenues, and remains the service category they would most actively need to defend,” it concludes.

Share