Mobile revenue in Africa will rise from $54.31 billion (R804 billion) in 2019, to $67.12 billion (R994 billion) in 2024.

This is according to the Africa Digital Outlook 2019 report from market research firm Ovum.

The research, which looks at the state of Africa’s telecommunications market, found data revenue on the continent will more than double in the next four years, from $14.91 billion in 2019 to $31.42 billion in 2024, growing at a significantly faster rate than voice calling.

However, due to the overall growth in the mobile market and continued relevance of voice calling for many customers, some major African operators, such as Airtel and MTN, will continue to see growth in mobile voice revenue, notes Ovum.

“Ovum expects mobile voice revenue in Africa to rise modestly through to 2021, but to decline thereafter to the end of the forecast period,” says Matthew Reed, practice leader at Ovum.

“Service providers are reporting strong growth in revenue from data access and digital services such as mobile money in Africa. Mobile broadband and financial services are key growth segments. The availability of affordable data-enabled devices is a key contributing factor to this growth in African markets, where average incomes are typically low.”

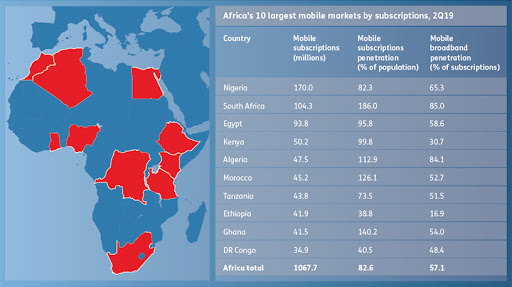

Mobile subscriptions in Africa passed the one billion mark in 2017, and reached about 1.07 billion in June 2019, with population penetration of 82.6%, according to Ovum.

Nigeria, the most populous country on the continent, also has Africa's biggest mobile market by subscriptions, with 170 million mobile subscriptions in 2Q19. The next-biggest markets are SA, with 104.3 million mobile subscriptions, and Egypt, with 93.8 million mobile subscriptions, and Kenya with 50.2 million.

Smart feature phone boost

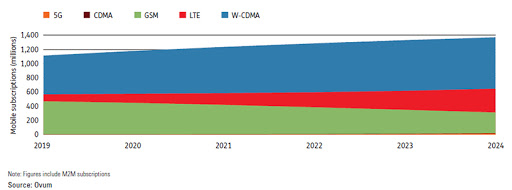

There will be 1.08 billion mobile broadband connections on the African continent by 2024, representing 79% of the 1.37 billion overall mobile connections on the continent, as service providers expand their mobile broadband networks, and as smart devices and services become more affordable, according to Ovum.

It adds the number of 3G W-CDMA connections in Africa will continue to increase through to 2024, in contrast with global trends, where these are expected to decline in other parts of the globe over the next few years.

“An overwhelming majority (85.3%) of mobile broadband connections on the continent were accounted for by 3G W-CDMA in the second quarter of 2019, while LTE accounted for just 14.2% of connections. 2G GSM still has a substantial market share, accounting for 42.9% of Africa's mobile connections in 2Q19,” notes the report.

However, it predicts 14.2% of mobile LTE connections on the continent are expected to increase at a more rapid rate, rising from 97.5 million at the end of 2019, to 336 million at the end of 2024.

“Both MTN and Orange have introduced smart feature phones that use the Kai operating system and are priced at about $20 as a means of encouraging wider take-up of data services,” Reed points out.

“Tecno, backed by Chinese company Transsion, has become one of the biggest mobile phone brands in Africa by offering affordable smartphones with features tailored to the African market, such as long-life batteries.”

Vodacom is also looking to extend its smart feature phones portfolio by bringing KaiOS-powered devices to the South African market in the second quarter of 2020.

The report warns instability, poor infrastructure and digital divide factors will continue to hold back digital development in Africa.

“Just one example of the barriers to digital development in Africa is that in 2018, the average cost of a 1GB mobile broadband plan on the continent was equivalent to 8% of average monthly income – far above the affordability benchmark of less than 2% of income, according to the UN Broadband Commission,” it notes.

Fixed broadband household penetration in Africa was about 8.5% at end-2Q19, lower than in any other world region, except Central and Southern Asia.

In terms of 5G connectivity, although SA’s two biggest operators, MTN and Vodacom, have been preparing for 5G for some time, it was data-only service provider Rain that became the first in the country to launch commercial 5G services when in September 2019 it started to offer 5G fixed-wireless home broadband in Johannesburg and Pretoria, with plans to expand to Cape Town, Durban and other cities.

“MTN and Vodacom say their plans to launch 5G in SA have been held up because they do not have access to the spectrum required in the sub-1GHz bands, as well as in the 2.6GHz and 3.5GHz bands. In 2018, Vodacom launched what it said was Africa's first commercial 5G service in Lesotho, using spectrum in the 3.5GHz band to which Vodacom has access in Lesotho but not in SA,” notes the report.

In the first week of November, the Independent Communications Authority of South Africa published the long-awaited information memorandum on the licensing process for the assignment of the International Mobile Telecommunications spectrum.

WiFi projects on the increase

WiFi networks are increasingly important for broadband connectivity in Africa. Facebook and Google both have WiFi ventures on the continent: Facebook's Express WiFi operates in Ghana, Kenya, Nigeria, SA, and Tanzania; and the Google Station WiFi service operates in Nigeria.

“There are also efforts to improve connectivity in rural areas, using a range of technologies. MTN Group is working with the Facebook-backed Telecom Infra Project to test and deploy low-cost wireless networks designed for rural areas. Loon, a subsidiary of Google's parent company Alphabet, is to run a trial with Telkom Kenya of its plan to use giant helium balloons to bring wireless broadband connectivity to remote areas,” according to the report.

Although wireline broadband penetration is low in Africa, Ovum expects the number of FTTx (fibre to the customer) subscriptions on the continent to grow strongly over the coming few years, from 1.28 million at end-2019, to 4.07 million at end-2024.

“At end-2024, SA will have 1.22 million FTTx subscriptions, making it the biggest FTTx market on the continent (by subscriptions), followed by Morocco, Algeria, Egypt, and Kenya, forecasts Ovum.”

Share